This one investment mistake is costing Americans $172 billion per year in retirement savings

It’s such an easy mistake to make that it could happen to nearly anyone (and I want to help you avoid it)

Time to read: 7:30

Here’s what I’ll cover (with links so you can jump ahead):

#1 - What the simple, yet costly mistake is.

#2 - Why so many people make the mistake.

#3 - What you can do to avoid making it yourself (with a framework on how to think about investing).

Investing for retirement is simple. In fact, it can be boiled down to a pretty simple equation:

[Money in + investment returns + time] - fees - taxes - behavioral mistakes = your retirement nest egg

But, as I always say, “it’s simple, but it ain’t easy.”

Research coming out of Vanguard recently found that people saving for retirement in their IRAs are making one simple but very costly mistake that is costing Americans more than $172 billion per year in retirement savings and wealth.

What’s the mistake?

Not investing their money.

That’s right, even after one year following a rollover from a company retirement plan, like a 401k, over 50% of IRA owners are still in cash.

Those numbers eventually go down, meaning more people invest, but very, very slowly.

Source: WSJ & Vanguard

No matter your age or time horizon until retirement, this is a scary reality for tens of thousands of people. And, if we extrapolate the data, this likely means millions of people are missing out on critical investment gains and, more importantly, savings that can make or break retirement.

In fact, by some reports there are almost 30 million left behind or lost 401ks holding almost $1.7 trillion. Imagine what’s happening in those accounts?

The scarier part is that younger generations overwhelmingly have more of their IRA money in cash. And when time in the market is critical to building meaningful wealth, they are at risk of losing out on decades of compounding growth in their accounts.

Why is this happening?

My take is that there are three main reasons why people aren’t investing their money:

#1 - Thinking IRAs are just like 401ks

It appears that the largest issue stems from people thinking their money will be automatically invested once it hits their IRA. The confusion comes from how their company retirement plans (e.g. a 401k) are managed.

Many retirement plans have default investments for people with accounts. This means that their money is automatically invested in a mutual fund (or similar investment) based on their age and expected retirement date.

So even if they forget to choose an investment option, they’re money is automatically invested for them.

When that money is moved to an IRA, there are no default investment options or automated investment plans in place. You (the account owner) is responsible for choosing how you invest your money. So if you do nothing, nothing happens and the money sits in cash or something equivalent to cash.

While this appears to be simple, it clearly isn’t that easy.

#2 - Overwhelmed by the number of investment options

Company retirement plans typically have a limited number of investment options. In my 20 year career as a financial advisor, I’d say I typically see between 15 and 20 investment options. There are certainly plans with more, but most offer a limited investment lineup.

While some people look at this and think it’s a disadvantage for retirement savers, the simple fact of keeping it simple is, in fact, a positive for many people. It’s both simple and easy.

When it comes to an IRA, you have thousands of choices. Picking one investment might feel easy. Picking a handful of investments and understanding what you own, how they work together, how diversified you are, the overall risk of the account, how this account integrates with everything else you have in other accounts … that can feel outright overwhelming.

If you give people too many choices, especially in places where they may lack expertise, they will choose to do nothing over taking action.

#3 - Simply forgetting the account even exists

There are a few principles I live by that relate to this story:

Simple is always better than complex.

Action always beats perfection.

Some account owners move the money to their IRA and simply forget that the account exists. This generally happens when they lack the experience or expertise to manage their own investments OR they have too many accounts and struggle to keep track of everything.

This is one reason I always recommend consolidation of accounts (in most cases). Simplifying your financial life will almost always lead to better outcomes. Some people will create complexity for the sake of complexity.

Trust me, simple beats complex and action trumps perfection (because we never really find perfection and never take action).

What should you do today?

If there’s one lesson in all of this that you can walk away with today it’s this:

Simple ideas, well executed > complex ideas never implemented

Now, more tactically, here’s what to do:

#1 - Take inventory of all of your investment accounts.

This is simple and easy. Make a list of every investment account that you have – 401k, IRA, Roth IRA, taxable account, education savings accounts, health savings account, and anything else.

Pull up the account online and/or pull up a recent statement and see how you are invested.

For the purposes of this exercise, as long as you aren’t in cash and you are invested you are OK (for now). I could go on about fees and taxes and your overall investment strategy, but that will have to wait for another article.

#2 - Keep investing simple.

Now, full disclosure, this is NOT investment advice. Why? Because I don’t know you and your situation. But here is a simple way to think about this. I am all about creating frameworks or mental models that we can apply for our financial lives.

And you’ll see that my framework is simple and easy because the most important thing is to take action.

If you are interested in learning more, my company and our Chief Investment Officer, Tom Graff, writes some really excellent educational content that you can find on our website. And, all of the content is completely free.

OK, back to my framework. I’m making up a percentage here, but I’d say 80% of the battle is just putting your money in something simple, low cost, and that invests broadly (i.e. that is diversified).

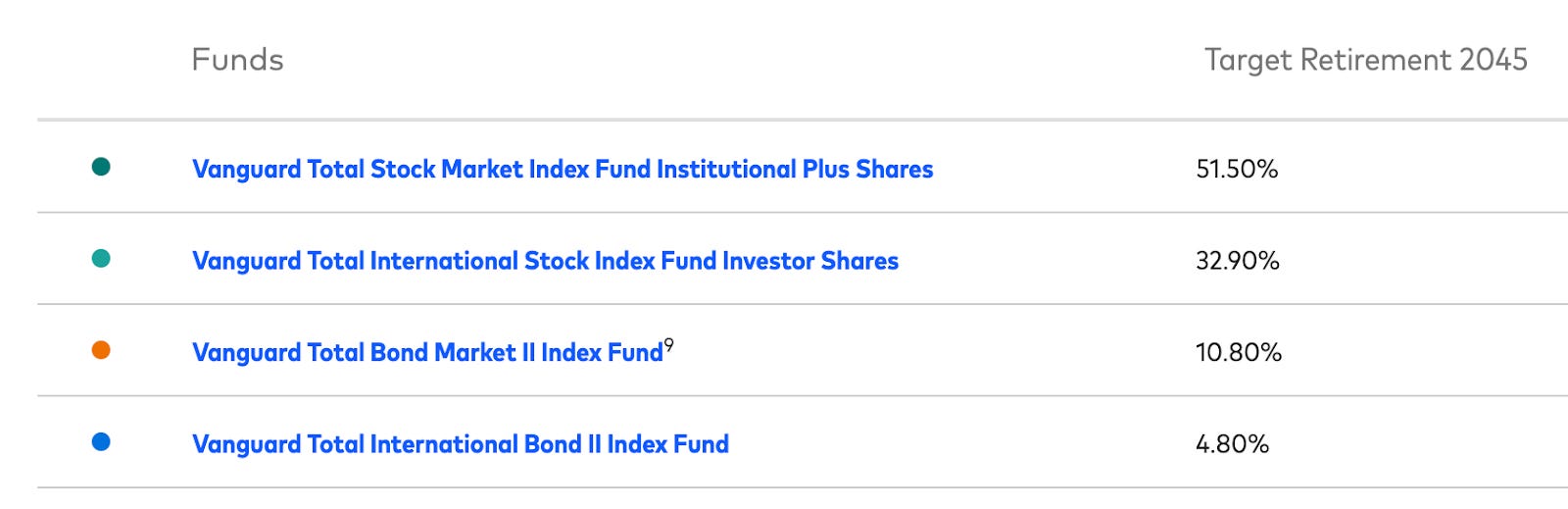

If I wasn’t a financial advisor and I didn’t have access to a team of experts at my own company, I’d put my money in a Vanguard Retirement Date fund. I picked the one that matches with my expected and “normal” retirement date for the visual below. That doesn’t make it right, but I’m sharing it as an example.

As you can see, it’s one investment that holds four individual Vanguard funds. It automatically divvies up the money and adjusts the percentages over time to gradually lower your risk until you reach retirement (i.e. it will adjust the stock to bond investments for you).

Essentially, you end up owning U.S. and international stocks and U.S. and international bonds. For full transparency, my larger investment accounts own something a little more sophisticated than this (plus they are invested through my company Facet), but my health savings account (HSA) is invested in these funds because it’s smaller and I want to keep it simple.

With this simple investment, you’ll own more than 10,000 companies around the world and have some of your money in bonds to balance the risk. And, also, think about how cool this is. You can become a business owner (without having to do the business owner stuff) overnight!

A closing thought to bring this home

This is an oversimplification of what you should be doing with your money. When I work with people in my capacity as a financial advisor, we never make a financial decision in a vacuum. The guidance I shared above is, to some extent, “vacuum advice.” So please know that all of this is shared to hopefully make this a little easier for you and to help you understand how to think through financial solutions.

Remember → Simple ideas, well executed > complex ideas never implemented.

The 80/20 rule works in many areas of personal finance. You can do 20% and get 80% of the results. However, the extra 80% of the work and 20% of the progress is where the real magic can happen.

There’s so much more you need to consider when it comes to creating and achieving financial success including how much you save, the account types you use, the investments you choose, the level of risk you take, the fees and taxes you pay (or don’t pay), and how you evolve your strategies as markets, the economy, and, more importantly, your life change.

And let’s not forget WHY you’re investing in the first place (i.e. what does money let you do?).

It’s never a bad idea to get expert advice. Yes, I am biased in my opinion since I am a financial advisor, but I truly believe it’s one of the best investments you can make (and not just a cost).

I have coaches or mentors for every aspect of my life – personal trainer (I’m also a Crossfit Level 1 Trainer), a life and career coach, and, yes, I even use a financial planner at my own company to help keep me on track. If you want to accelerate your path to success, working with a coach or expert advisor can be a great way to do it.

At the end of the day, the one thing I want is for you, and everyone else, to reach their full financial potential and to use that potential to lead a more fulfilling life.

How you do that … well, that’s your decision. No matter your choice, I wish you the best in your journey.

Cheers to health, wealth, and the good (financial) life,

Brent